This PDF is a selection from an out-of-print volume from the National

Bureau of Economic Research

Volume Title: Business Finance and Banking

Volume Author/Editor: Neil H. Jacoby and Raymond J. Saulnier

Volume Publisher: NBER

Volume ISBN: 0-870-14137-6

Volume URL: http://www.nber.org/books/jaco47-1

Publication Date: 1947

Chapter Title: Commercial Banks as Suppliers of Credit to Nonfinancial

Business: 1940

Chapter Author: Neil H. Jacoby, Raymond J. Saulnier

Chapter URL: http://www.nber.org/chapters/c4683

Chapter pages in book: (p. 38 - 68)

Chapter 2

.BANKS AS

SUPPLIERS OF CREDIT TO NONFINANCIAL

BUSINESS: 1940

IT IS USEFUL TO THINK of the American business credit market as

being composed of two divisions, one concerned with short-term

credit running for one year or less, and the other with medium-

term and long-term credit running more than one year to maturity.

The principal forms of short-term credit appearing on business

balance sheets are accounts payable and notes payable due in one

year or less, while the major forms of medium-term and long-

term credit are term loans due in more than one year, bonds, deben-

tures, and mortgage lOans. Each class of indebtedness represents

obligations due to a variety of creditors. In 1940 commercial banks

were an important source of medium- 'and long-term as well as of

short-term business credit, although they were not the ma] or source

of either type of credit.

SHORT-TERM VERSUS MEDIUM-TERM AND

LONG-TERM BUSINESS CREDIT

While the technical distinction between medium- and long-term

and short-term

is based upon the term to maturity of the

loan, one year being the dividing line, the true economic distinc-

tion is grounded on the nature of the business transaction being

financed. For example, businesses whose operations are subject to

strong seasonal influences are ordinarily large users of short-term

credit obtained to finance seasonal bulges in their operations. In

practice, however, there is no sharp divergence in the uses to which

either class of credit is put by business concerns. Loans that are

technically of short term may be used to finance fixed assets or long-

sustained operations, and medium- and long-term loans may be

used in part to finance temporary transactions.

BANKS AS SUPPLIERS OF CREDIT, 1940

39

Both loan markets are characterized by competition among par-

ticular sets of credit agencies. The two markets differ in credit

appraisal methods and standards. In lending on short term, credit

institutions tend to place greater reliance on the balance sheet of the

borrowing business in order to determine whether liquidation of

current "trading" assets is likely to produce sufficient funds to pay

off the debt. In lending on medium or long term, greater emphasis

is given to the earning power of the concern over a period of years,

and its ability to "throw off" cash to service the debt.

In 1939 the short-term debt (defined here as equivalent to the

current

liabilities) of all American nonfinancial corporations

amounted to $23 billion on a nonconsolidated basis.1 Their gross

outstanding long-term debt, on the other hand, was

billion, or

about 45

percent more than the short-term obligations. More than

half of the short-term debt was owed by manufacturing and trad—

ing. concerns; nearly nine-tenths of it by these corporations plus

public utility companies (including railroads). As for long-term

debt, more than 70 percent was owed by railroad and other public

utility companies, whose assets consisted of fixed property.

Data for 1937 indicate that the proportion of assets financed by

short-term debt declined quite sharply as size of corporation in-

creased up to businesses having total assets of

million. But this

tendency for the importance of short-term debt to shrink with in-

creasing size of business was not offset by an expansion of the ratio

of long-term debt to total assets, except among large businesses

with total assets of $,ç million and more, and among public utility

companies. As between profitable and unprofitable corporations,

variation in the use of short-term debt was very striking, the ratio

•

' Short-term

and long-term business credit outstanding at any time can be measured

only imperfectly. First, credits written to run a year or less are renewed frequently,

and may be regarded by both borrower and lender as long-term loans. This produces a

bias toward understatement of real long-term credit in available financial statistics.

Second, business concerns customarily include among their current liabilities those

instalments of a long-term debt that fall due within the ensuing fiscal year. This in-

troduces a bias in the opposite direction. Third, short-term debt at statement date may

be less than the year's peak because of the tendency to repay loans at that time and to

use a fiscal year ending in a period during which short-term credit needs are at a

minimum. Finally, business balance sheets fail to classify either short- or long-term

debts as between types of creditors, which precludes direct measurement of their rela-

tive importance. While "accounts payable" may be presumed to measure debt due to

trade suppliers, "notes payable" cover debt due to commercial banks, commercial finance

companies, affiliated companies, trade suppliers, stockholders, or other agencies.

40 BUSINESS FINANCE AND BANKING

of current liabilities to total assets for unprofitable businesses being

40 to 50 percent higher than for profitable concerns.

What general explanation can be offered for the particular ma-

turity distributions of debt found among business enterprises? Why

do business concerns not borrow entirely on short term or entirely

on long term?

Part of the answer to this question is provided by a study of the

kinds of assets employed by businesses and their variability in value

through time. Long-term credit demands are related to the owner-

ship of fixed property, and short-term credit requirements are

related to the volume of current assets and transactions. If the

technology of a business is such that the amount of its assets varies

considerably within short periods —

a

probable situation where

current assets form a large proportion of total assets —

the

use of

short-term debt is likely to be relatively larger than where total

assets are comparatively stable. But the correlation of large current

debt with large current assets in various industries is so imperfect

as to

indicate that the term structure of business debt is far from

being controlled by the term structure of assets. The considerations

affecting the division of the debt of a particular concern between

short- and long-term obligations are not easily fitted into a neat

formula. They may be described, in general, as considerations of

technology, alternative cost, urgency, and flexibility.

SOURCES OF SHORT-TERM CREDIT TO BUSINESS

Three categories of short-term business liabilities can be distin-

guished: trade credit obtained by a concern from other businesses

that supply it with inventories or, less frequently, with machinery

or equipment; commercial credit obtained from banks, finance

companies, governmental loan agencies, or other financial institu-

tions; "other" current liabilities represented by the accrued obliga-

tions of a concern to tax collectors, insurance companies, or other

agencies, and notes due to owners, stockholders, or other nonpro-

fessional lenders. The significance of this division lies in the differ-

ence in the terms upon which each type is available and in the

circumstances of its use. Trade credit is associated directly with the

purchaseof merchandise or services; commercial credit involves the

formation of a relationship with a lending institution in the financial

Industrial

Division

.

Trade Debt Bank Debt

Amounts Due

Individuals

.

Chattel

Mortgages

Miscellaneous

Current

Liabilities

A ccrued

Liabilities

Total Current

Liabilities

Manufacturing 42.9%

17.2%

13.6%

i.o%

'9.7%

ioo.o%

Wholesale trade 64.0

18.5 10.5

.4

2.9

3.7

100.0

Retail trade

40.8

17.5 11.2

100.0

Construction

57.5

- 16.3

11.3

.5

7.7

6.7

100.0

Service

31.5

17.7

10.5

59.4

7.3

13.6 100.0

COMBINED

44.0%

17.4%

5.7%

14.8%

a Based

on data in Carl Kaysen, Industrial and Commercial Debt —

A

Balance Sheet Analysis, 1939 (National Bureau of Economic

Research, Financial Research Program, ms. 1942)

Table

A-i, which was compiled from a sample of about 6,200 concerns.

C.)

'0

Table —

ESTIMATED PERCENTAGE DIs'riuBuTloN OF CURRENT LIABILITY ITEMS OF

NONFINANCIAL BUSINESS CONCERNS, BY MAJOR INDUSTRIAL DIvIsIoNs, 1939a

in

(I,

U,

'0

'0

t-.

in

In

0

"1

42

BUSINESS FINANCE AND BANKING

market; "other" current liabilities involve loans from agencies

likely to be influenced by special considerations in assuming a

creditorship position, and accrued expenses, such as taxes or insur-

ance, chargeable to past operations but not yet due.

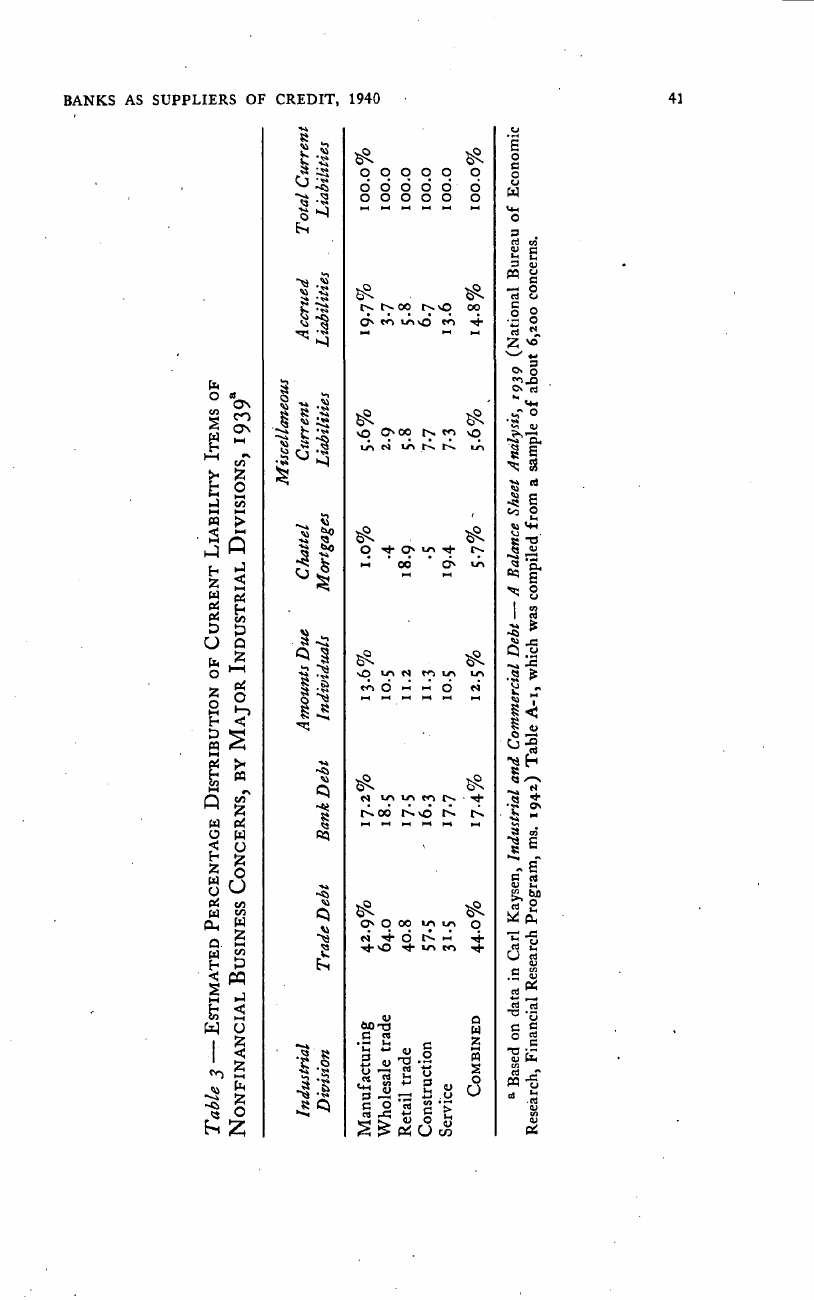

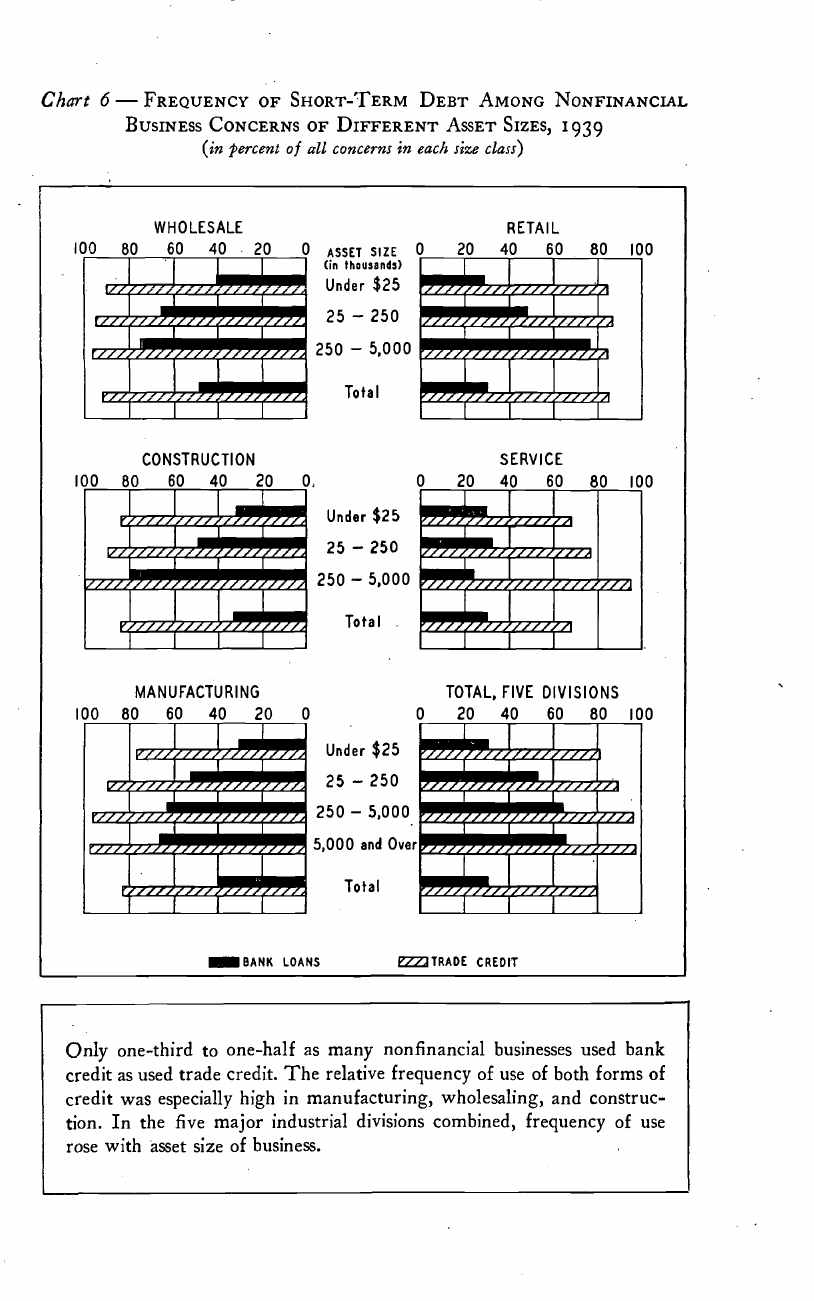

PREPONDERANCE OF TRADE CREDIT

Quantitatively trade credit is the most important type of short-

term business credit in every major industrial division of the non—

financial economy (Table 3). In 1939 trade debt was about two and

one-half times as large as bank debt for manufacturing, trade, con-

struction, and service industries combined.2

Furthermore, because of its role in current transactions, trade

credit is found in the balance sheets of businesses with far greater

frequency than is bank credit (Chart 6). Irrespective of size, degree

of profitability, or kind of industry, an overwhelming majority of

businesses showed accounts payable on their balance sheets at the

end of 1939:in wholesaling, 92 percent; in manufacturing, 83 per-

cent; in retail trade,

percent; in construction, 84 percents and in

the service industries, 68 percent. The frequency of use of trade

credit rose steadily with size of concern in all ma] or industrial

groups, probably because big businesses purchased on credit from

a larger number of suppliers than did small concerns and were more

likely to be using some trade credit at any given time.

While perhaps 8o percent, or 2.7 million, of the 3.4 million non-

financial businesses at the outbreak of World War II had outstand-

ing trade debt, only about 35 percent, or not more than 1.2 million,

of them had outstanding debt to financial institutions — mainly

to commercial banks. Because, as indicated above, the ratio of trade

debt to bank debt was approrimately two and one-half times in

manufacturing, trade, construction, and service industries combined,

2

Debt to business

suppliers outweighed bank debt by 3.6 to

i in

construction; in

wholesaling the ratio was 3.4, in retaiitng z.S, in manufacturing in service 1.7,

and for all live divisions combined it was z.6. See Carl Kaysen, Industrial and

inerdal Debt — A

Balance Sheet Analysis (National Bureau of Economic Research, Fi-

nancial Research Program, ms. i942)

p.

30.

For public utilities and extractive indus-

tries the data suggest that trade credit was more than double the amount of outstand-

ing bank credit. See Sidney S. Alexander, Changes in the Financial Structure of

can Business Enterprise, 1900—1940 (National Bureau of Economic Research, Finan-

cial Research Program, ms. 1943) Table 9, p. V-S. Unfortunately, Alexander's data

compare accounts payable with notes payable, and a substantial fraction of the latter

evidences debts owed to agencies other than banks.

44

BUSINESS FINANCE AND BANKING

it appears that for the average business utilizing both types of

funds the average amount of trade credit was in excess

of the amount of its lank loans. For the major industrial divisions,

there was substantial correlation between the frequency of use of

trade credit and of bank credit. This correlation suggests that bank

borrowing was used by business management in most cases to sup-

plement . other

sources of short-term credit, and not to substitute

for that obtained from business suppliers.

What is the explanation of the fact that about two and one-half

times as many businesses used trade credit as used bank credit, and in

amounts about two and one-half times as large? The answer is

not simple.. A substantial

. part

of outstanding trade credit was

representing sums due to trade suppliers which were in

process of payment at the time balance sheets were drawn. A con-

siderable amount of trade debt was also incurred more or less

"automatically" by business managements as a matter of purchasing

convenience, and in the case of unprofitable concerns as a matter of

necessity. Apart from these factors, the relative uses of trade credit

and bank credit appear to have been related to the size, industry,

and technology of business concerns. Thus large concerns (i.e., chain

stores and mail-order houses) purchasing from small suppliers

tended to have low levels of accounts payable, as did concerns

purchasing standardized commodities in well-organized markets

(i.e., millers, meat packers, and tobacco manufacturers). Never-

theless, taking the economy as a whole, industries .that used rela-

tively large amounts of trade credit also used relatively large

amounts of short-term bank credit, indicating the existence, com-

mented upon above, of a complementary rather than a competitive

relationship between the two sources of credit.

BUSINESSES USING SHORT-TERM BANK CREDIT

A telescopic view of the short-term business borrowing clientele of

commercial banks around 1940 would result in the "typical" bor-

rower being described roughly in these terms: It was a small or

medium-sized manufacturing or trading concern, of somewhat less

than average profitability, which tended to borrow repeatedly in a

succession of years.

While there is no direct information on the industrial distribu-

BANKS AS SUPPLIERS OF CREDIT, 1940

45

tion of short-term bank credit around 1940, collateral information

from several

leads• to the conclusion that manufacturing

and trading enterprises were the two most important categories of

business

borrowers from commercial

banks.

Together they

accounted for more than half of all outstanding "commercial and

industrial" loans. Miscellaneous finance companies — mainly per-

sonal loan and sales finance organizations —

accounted

for another

sixth to a quarter of these loans; public utility concerns for an addi-

tional i 5—so

percent;

and the balance were scattered among serv-

ice, construction, and miscellaneous industries..

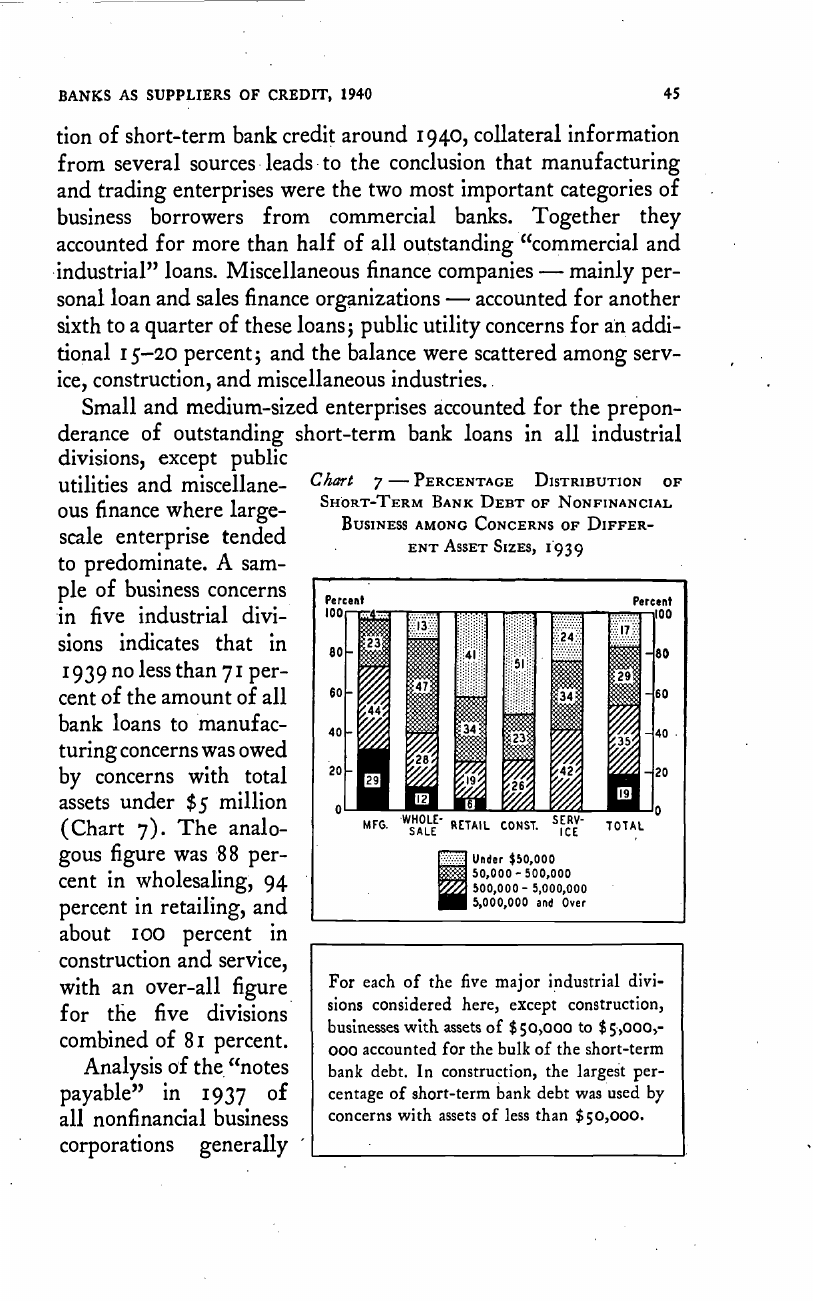

Small and medium-sized enterprises accounted for the prepon-

derance of outstanding short-term bank loans in all industrial

divisions, except public

utilities and miscellane-

Chart

7

— PERCENTAGE

DISTRIBUTION

OF

ous finance where large-

SHORT-TERM BANIC DEBT OF NONFINANCIAL

BUSINESS AMONG CONCERNS OF DIFFER-

scale enterprise tended

. ENT ASSET SIZES, 1939

to predominate. A sam-

pie of business concerns

five industrial divi-

sions

indicates that

in

1939 no less than 71 per-

cent of the amount of all

bank loans to manufac-

turing concerns was owed

by concerns with total

assets under

million

(Chart 7). The analo—

gous figure was 88 per-

cent in wholesaling, 94

percent in retailing, and

about

100 percent in

________________________________

construction

and service,

with an over-all figure

For each of the five major industrial divi-

r p i. • . sions

considered here, except construction,

ior tne nve aivisions

bustuesses with assets of $50,000 to $ 5,000,-

combined of 81 percent.

000 accounted for the bulk of the short-term

Analysis of the. "notes

bank debt. In construction, the largest per-

payable"

in

1937

of

centage of short-term bank debt was used by

all nonfinancial business

concerns with assets of less than $50,000.

corporations generally

46

BUSINESS FINANCE AND BANKING

confirms the view that "big business" was a minor element in the

short-term credit clientele of banks, small and medium-sized cor-

porations with assets under $5

million accounting for 6i percent of

all notes payable, although oniy 30 percent of corporate assets and

53

percent

of corporate sales were attributable to this group. A sur-

vey of commercial and industrial loans made by Federal Reserve

member banks during one month of 1942 shows that 71 percent of

the amount of such loans went to small and medium-sized busi-

nesses.

Unprofitable businesses showed relatively larger amounts of

bank credit on their balance sheets than did profitable concerns, both

because losses reduced equity and automatically increased the rela-

tive importance of bank debt, and because lack of profits reduced the

ability to pay off outstanding bank debt. Nearly 6o percent of all

nonfinancial corporations. reported no taxable net income during

1937. These concerns accounted for but 22 percent of the gross

income of all corporations in that year, but they owed 43 percent of

the amount of notes payable.8 The percentages of notes payable to

total assets at the end of 1937, for income and deficit corporations of

different sizes, reveal a markedly greater indebtedness for small

than for large corporations, as well as heavier indebtedness for the

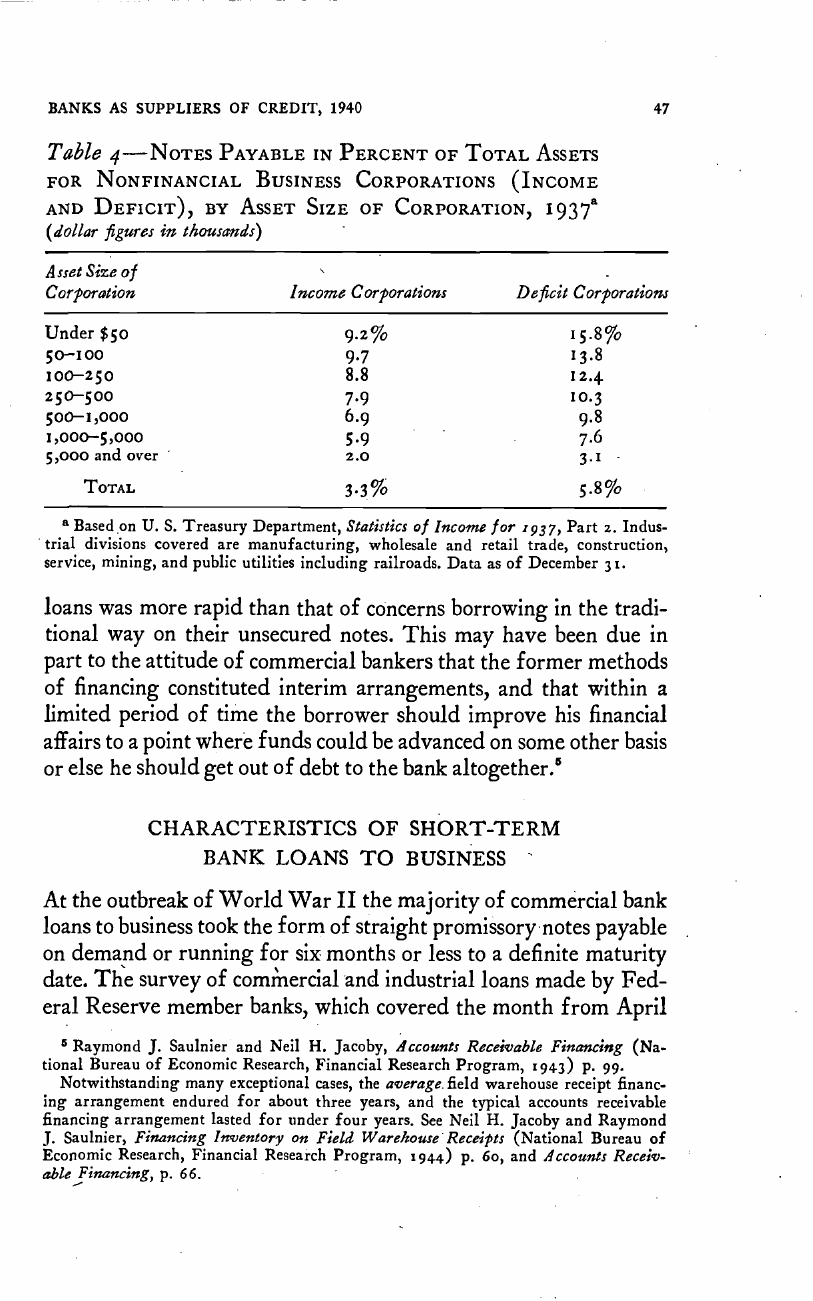

unprofitable businesses of each size-group (Table 4).

Roughly two-thirds of the business concerns receiving credit

from a bank at a given time might have been expected to be in its

debt during the following year according to 1939 data for a sample

of companies. This may be inferred from the fact that 64 percent

of the sample indebted to banks were either "steady" or "sea-

sonal" borrowers, while only 36 percent were bor-

rowers.4 Among manufacturing, wholesaling, and retailing con-

cerns the proportion of "steady" bank borrowers rose with size

of concern. The turnover of businesses pledging their accounts

receivable, equipment, or inventories as collateral security for bank

In Statistics of Income for '937, Part it is reported that 192,028 corporations,

or 40 percent of the total active corporations, filed returns showing net incomeln 1937,

while z8g,Sio corporations, or 6o percent, filed returns showing no net income. The

income corporations had total gross income of $109 billion or 77 percent of all cor-

porate gross income, while the no-income corporations had $33 billion of gross income

or 23

percent of the total.

It would be valuable to know to what

turnover in the borrowing clientele

of commercial banks results from (z) business birth or discontinuance and (z) im-

provement or deterioration in the financial status of continuing enterprises. Both

factors play a part, but the importance of each cannot be measured from existing data.

BANKS AS SUPPLIERS OF CREDIT, 1940

47

Table 4—NOTES PAYABLE IN PERCENT OF TOTAL ASSETS

FOR NONFINANCIAL BUSINESS CORPORATIONS (INcoME

DEFICIT), BY ASSET SIZE OF CORPORATION,

(dollar

figures in thousands)

Asset Size of

Corporation Income Corporations Deficit Corpora/ions

Under 9.2%

50—100

9.7

13.8

100—250

8.8 12.4

250—500

7.9

10.3

6.9

9.8

1,000-5,000

5.9 .

. 7.6

5,000 and over

2.0

3.1 -

TOTAL

3.3%

a Based

on U. S. Treasury Department, Statistics of Income for 1937,

Part

z. Indus-

trial divisions covered are manufacturing, wholesale and retail trade, construction,

service, mining, and public utilities including railroads. Data as of December 31.

loans was more rapid than that of concerns borrowing in the tradi-

tional way on their unsecured notes. This may have been due in

part to the attitude of commercial bankers that the former methods

of financing constituted interim arrangements, and that within a

limited period of time the borrower should improve his financial

affairs to a point where funds could be advanced on some other basis

or else he should get out of debt to the bank altogether.5

CHARACTERISTICS OF SHORT-TERM

BANK LOANS TO BUSINESS

At the outbreak of World War lithe majority of commercial bank

loans to business took the form of straight promissory-notes payable

on demand or running for six months or less to a definite maturity

date. The survey of comr'nercial and industrial loans made by Fed-

eral Reserve member banks, which covered the month from April

Raymond J. Saulnier and Neil H. Jacoby, Accounts Receivable Financing (Na-

tional Bureau of Economic Research, Financial Research Program, 1943) p. 99.

Notwithstanding many exceptional cases, the average, field warehouse receipt financ-

ing arrangement endured for about three years, and the typical accounts receivable

financing arrangement lasted for under four years. See Neil H. Jacoby and Raymond

J. Saulnier, Financing Inven€ory on Field Warehouse 'Receipts (National Bureau of

Economic Research, Financial Research Program, 1944) p. 6o, and ..4ccounts Receiv-

able Fimzncing, p. 66.

48 BUSINESS FINANCE AND BANKING

r 6 to May 15, 1942, indicates that the 90-day note was the principal

basis of short-term debt to banks. The average maturity of loans is,

of course, a misleading measure of the average length of time any

individual business is continuously in debt to a bank, because many

bank loans are renewed successively, the borrower paying off part

or all of an old note with the proceeds of a new one. Inasmuch

as 41 percent of the total loan volume of the one month surveyed

was accounted for by renewals of old loans, it would appear that the

majority of loans were renewed in whole or in part at their average

maturity of 90 days.

Apart from advances against demand or short-term notes, banks

and commercial finance companies also entered into credit relation-

ships with business which were short term in form but long term in

actual duration, because of a "revolving credit" feature. The prin-

cipal illustrations are loans secured by business accounts receivable,

loans secured by warehouse receipts arising from the deposit of mer-

chandise in a field warehouse on the premises of the borrowing

business, and the financing of commercial and industrial equipment

on instalment terms. These newer "short-term" business credit

forms, which are described in Chapter 5, more directly recognize

the actual duration of business credit requirements than does the

traditional short-term commercial loan.

In both number and amount,

of short-term bank

loans to business in 1939 were not collaterally secured by liens on

business assets. They involved "open" credits, based on the finan-

cial worth and reputation of the borrowing enterprise or its princi-

pals and carrying only their promises to make repayment. Only 20

percent of all enterprises in five industrial divisions that borrowed

from commercial banks in that year provided collateral security.

Service industries most frequently provided liens on assets (in 43

percent of the cases), probably because many businesses such as

garages and repair shops purchased equipment on conditional sales

contracts or under chattel mortgages. Retail concerns furnished

liens on assets in 26 percent of the cases, construction in 2o percent,

manufacturing in 20 percent, and wholesale trade in ii percent.

Probably less than 20 percent of the $6,671 million of "commercial

and industrial" loans held by operating insured commercial banks

in the United States at the end of 1940 were collaterally secured.6

Commercial and industrial loans on this date probably included about $2,162•

million of term loans, which were not short-term credits, and about one-third of

BANKS AS SUPPLIERS OF CREDIT, 1940

49

While the newer forms of short-term business credit extended by

banks involve collateral security, they constitute a minor part of

total bank credit. The preponderance of business loans of commer-

cial finance companies, it should be observed, are collaterally

secured business loans.

Only a minor proportion of unsecured bank loans to business

concerns in 1939 carried the endorsement of others than the bor-

rower, thus providing the lending institutions with additional secu-

rity. About percent of the unsecured loans to manufacturing

concerns were endorsed, 31 percent in wholesale trade, 26 percent

in retail trade and in construction, and 7 percent in service indus-

tries. Among small corporations especially, principal stockholders

or officers were often required to endorse the notes given by their

companies. To the extent that this occurred, the limited liability

otherwise enjoyed by owners of corporations partly disappeared.

INTEREST CHARGED ON SHORT-TERM.

BANK LOANS

The effective annual interest rates — including any special service

fees —

charged for business credits around 1940 were determined

by the size of the loan, the amount of risk of non-repayment

attached to the loan, and the character of the financing plan.

From the point of view of the lending institution, the major

element in the charge was not "pure" interest, or the return on

loan assets with short maturities, for which the yield (e.g.,

on high-grade commercial paper) was under i percent at that

time; it was the expense of loan administration and the premium

for risk of nonrepayment. In making a loan of any amount, a bank

incurs certain "fixed" costs in investigating the applicant and

appraising his financial worth and prospects. When these expenses

are spread over a small loan, the charge per dollar' is necessarily

higher than when they are spread over a large loan. Moreover, the

risks of lending to small ventures are typically greater, because the

average profit rate is lower and less stable than for large businesses.

According to the Federal Reserve member bank survey made in

1942, interest rates charged on business loans averaged 3.4 percent.

which were collaterally secured. See Neil H. Jacoby and Raymond J. Saulnier, Term

Lending to Business (National Bureau of Economic Research, Financial Research

Program, 1942) pp. 3o,

and

SO

BUSINESS FINANCE AND BANKING

But the rate ranged from percent on loans to the smallest class

of borrowing businesses to 1.8 percent

on loans made to the largest

dass of concerns. Industrial variations in loan rates, which roughly

measure differences in the risk of investment in various fields, were

also quite marked. Finally, collateral loans carried substantially

higher charges than did unsecured loans, because the charge had to

cover the additional expense of appraising and handling the col-

lateral security.

Charges by commercial banks on accounts receivable loans ran

between 6 and 9 percent per annum during 1941. Commercial

finance companies, which generally assumed somewhat larger credit

risks and incurred greater administrative expenses in lending

against accounts receivable, charged rates running between 9 and

20 percent. Loans secured by field -warehouse receipts, which were

made by both banks and commercial finance companies, involved

credit costs ranging from 4 to 10 percent. In financing business

equipment on instalment terms, lending institutions appear to have

charged between 5 and 7 percent.

NATIONAL CHARACTER OF SHORT-TERM

CREDIT MARKET

The degree of uniformity in the characteristics of short-term busi-

ness credit in different parts of the United States in 1940 reflected

a credit market more national in character than is often assumed.

At the outbreak of World War II, a business concern of given size

and industry would probably have used credit of about the same

maturity, employed it for about the same purposes, paid about the

same charge for it, and provided the same type of collateral secu-

rity, whether the concern was located in Boston, Chicago, or Seattle.

The policies of business managements in the use of short-term

credit did not vary significantly over the nation.7 Those regional

differences in loan characteristics that did exist were attributable

in large part to differences in the size and industrial affiliations of

businesses in different regions. For example, geographical varia-

tions in the use of the newer collateralized business loans clearly

It has been found that in 1939 "The pattern of credit use

.

appears to have

little connection

with .

. geographic location and population size of location

centre." See Carl Kaysen,

cit., p.

39.

BANKS AS SUPPLIERS OF CREDIT, 1940

51

reflected differences in the economic resources of the several

regions. Lending on field warehouse receipts was used with more

than average frequency in the Pacific area, where it is particularly

adapted to the canning and lumbering industries. Accounts receiv-

able financing flourished in the Atlantic states, where the textile

industries are important. For even the cost of bank credit, the evi-

dence indicates that a considerable fraction of the wide spread of

average interest rates charged business concerns in different regions

can be resolved into regional variations in the

size or in-

dustrial affiliation of borrowers.8 Regional differences in inter-

est rates — particularly

those charged by very small banks to very

small businesses

also

reflect other factors, such as differences

among regions in the costs of money to the banks.

SOURCES OF MEDIUM-TERM AND LONG-TERM

CREDIT TO BUSINESS

Medium-term and long-term business credit running more than

one year to maturity has taken two broad forms in the United

States: direct loans obtained by personal negotiation with lenders

and including such types as term loans, priyate placements of bonds,

notes or debentures, and mortgage loans;

market

loans ob-

tained through public offerings of debt securities, in which the

services of investment underwriters and dealers are ordinarily

utilized as intermediaries between borrowing concerns and their

creditors —

the

ultimate security holders. In 1940 commercial

banks engaged in both direct lending on medium term and the

purchas.e in the open market of medium- and long-term corporate

securities for investment account. As grantors of medium- and

long-term business credit, banks competed with a set of lending

agencies different from those they faced in the short-term credit

market, and, to a considerable extent, they served larger businesses.

In obtaining medium- and long-term credit, the business com-

munity made use of direct loans with much greater frequency than

open market loans. Of the 650 thousand concerns estimated to have

outstanding medium- and long-term debt in 1940, only about 3.2

thousand, or 3/2 of i percent, had publicly distributed debt secu-

See Federal

Reserve Bulletin, November 1942,

p. IoS9.

0

52

BUSINESS FINANCE AND BANKING

rities outstanding. The remaining 99.5 percent had negotiated

their loans directly with a financial institution, an affiliated business

concern, or an individual. Only a minor fraction of the number of

such direct loans could be traced to a particular type of creditor. It

is known that up to the end of 1940 the government loan agencies,

comprising the Reconstruction Finance Corporation and the Fed-

eral Reserve banks, had granted term loans to about i i thousand

enterprises. In addition, commercial banks and the largest life insur-

ance

had lent directly to about 3.8 thousand businesses.

Apparently hundreds of thousands of small and medium-sized con-

cerns had obtained medium- and long-term cre4it from individual

capitalists, local insurance companies, savings banks, savings and

loan associations, investment companies, trust funds, nonprofit or-

ganizations, or other business enterprises.

The amount of the gross long-term debt of all corporations at

the end of 1940 was about $52 billion. Approximately $83 billion

represented debts owed to other corporations, indicating the great

extent to which businesses were financing each other through long-

term loans. As for the balance of these obligations, life insurance

companies were the most important holders, their portfolios of

long-term debt securities amounting to approximately $io billion.

Commercial banks ranked next, with holdings of about $.g.i billion

made up of $2.2 billion of term loans, $2.4 billion

of marketable

securities of business corporations, and about $çoo million of mort-

gage loans to industry. Mutual savings banks held about $'i billion

of corp orate bonds and notes, and the Reconstruction Finance Cor-

poration had outstanding loans to nonfinancial businesses amount-

ing to $599 million.

After deduction of these known repositories

of long-term corporate debt from the total, $27 billion remained to

be accounted for. Presumably, this balance represented the out-

standing long-term business credits extended by other sources, as

mentioned above.

BUSINESSES USING MEDIUM-TERM AND

LONG-TERM CREDIT

The 65o thousand American business enterprises that owed me-

dium- and long-term debt at the beginning of World War II may

be compared with the more than

million concerns that were in-

BANKS AS SUPPLIERS OF CREDIT, 1940

53

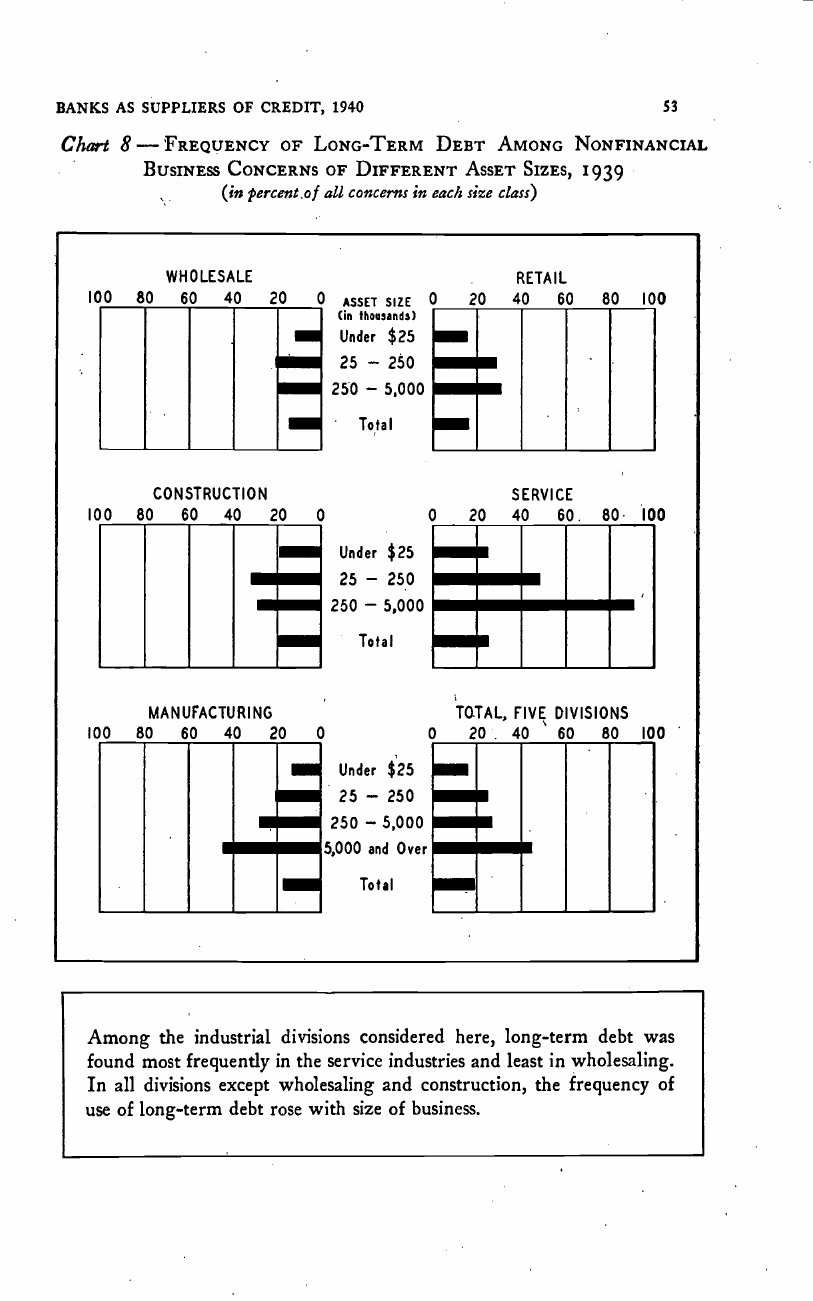

Chart 8 — FREQUENCY

OF LONG-TERM DEBT AMONG

BUSINESS CONCERNS OF DIFFERENT ASSET SIZES,

(in percent of all concerns in each size class)

NON F! NAN CML

'939

WHOLESALE

100

80 60 40

20

0

ASSET SIZE

(in thousands)

Under $25

25 — 250

250 — 5,000

RETAIL

20

40

60

CONSTRUCTION

100

80

60

40

—

.

I

.

I

0 80 100

. -.

—

To,t a I

SE RV I CE

0 20

40 60. 80• 100

Under

25 —

250 —

$25

250

5,000

_____ _____ _____

20

0

MANUFACTURING

100

80 60 40

20 0

I

—,

I

FIVE

0

20. 40

Total

Under $25

25 — 250

250 —

5,000 and Over

Total

DIV IS IONS

60

80 00

—

.

. U

Among the industrial divisions considered here, long-term debt was

found most frequently in the service industries and least in wholesaling.

In all divisions except wholesaling and construction, the frequency of

use of long-term debt rose with size of business.

54 BUSINESS FINANCE AND BANKING

debted on short-term account. Among large corporations, only 44

percent had long-term debt in 1937. Such debt was least frequent

among the extractive industries (26 percent of the concerns),

higher in manufacturing percent), still higher in trade

• percent), and well-nigh universal among public utility corpora-

tions, 99 percent of which had such obligations. These figures gen-

•

erally bear out the theory that long-term debt, which imposes an

annual fixed charge on earnings, is incurred most often by con-

cerns having the greatest stability in earning power.

Among corporations of different sizes in the five ma] or industrial

divisions studied, less than one-fifth of those with total assets under

$25 thousand showed long-term debt on their balance sheets in

1939 (Chart 8). But as asset-size of business increased the per-

centage of businesses having such debt rose, and 8o percent of the

• industrial giants with assets of $çoo million or more were so in-

debted.9 The marked rise in the use of long-term debt with size of

enterprise probably reflected the increasing availability of such

credit as the average profit rate rose and as annual earning power

became more stable. It may also have resulted from a financial

policy of business management not to commit the earnings of future

years until there was a high probability that the commitment could

•

be met without difficulty.

The businesses to which banks and life insurance companies

granted the bulk of their medium- and long-term credit differed

considerably from those served by the Reconstruction Finance Cor-

•

poration and the Federal Reserve banks. As shown by Chart 9, these

public lending agencies on the whole did not compete extensively

with the private institutions in regard to the size of medium-term

business loans made; and this absence of extensive competition with

respect to size of loan reflects a similar condition with respect to size

of business served.'°

For all types of lending institutions, manufacturing businesses

were the most important class of recipients of term loans (Chart

The low frequency of. long-term debt among small manufacturing corporations

was confirmed by C. L. Merwin, who found that only 26 percent of a sample of 1,300

such concerns with total assets under $z5o thousand had outstanding bonds or mort-

gages in 1936. Temporary

National Economic Committee,

Characteristics

of Small Manufacturing Corporations (Monog. 15, Washington, 194 i) pp. iio—iz.

10 See Term Lending to Business, op. Cit., p. 36.

BANKS AS SUPPLIERS OF CREDIT, 1940

55

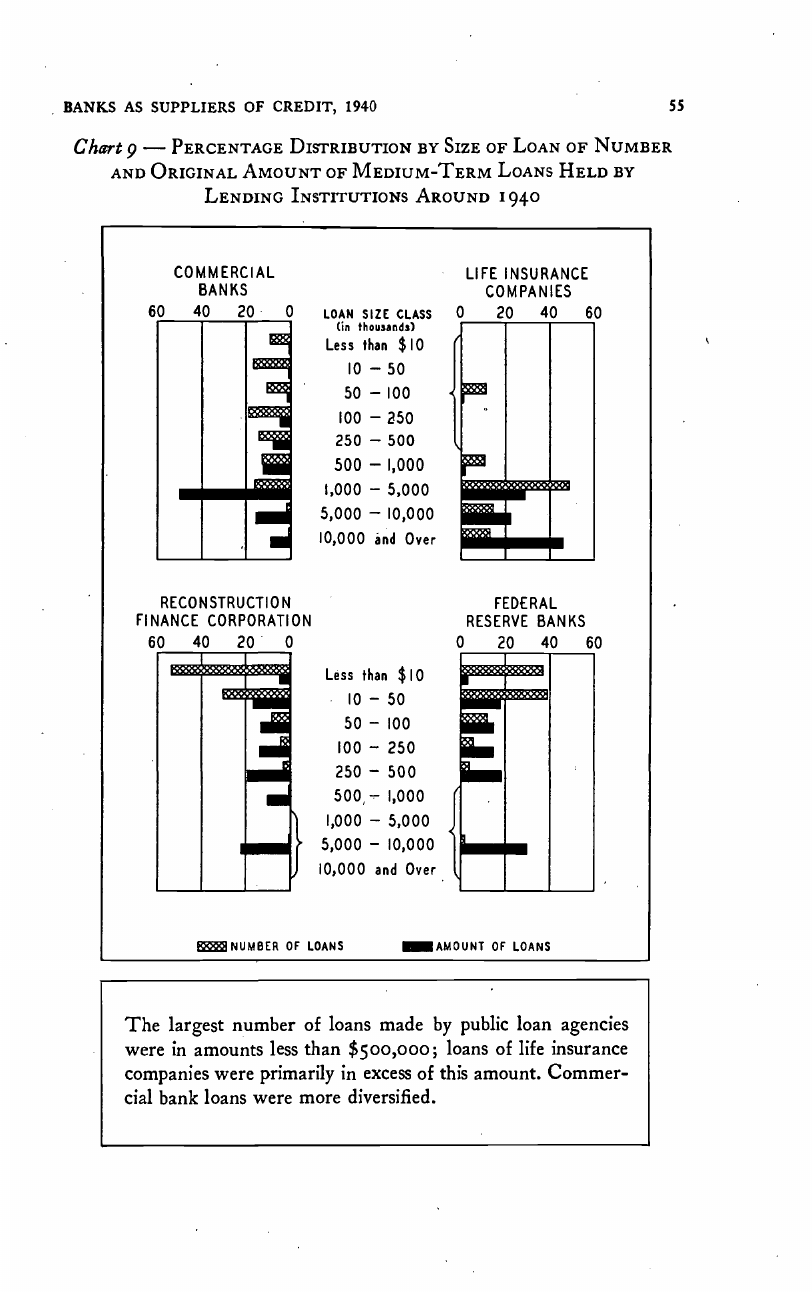

C

hart ç

— PERCENTAGE

DISTRIBUTION BY SIZE OF LOAN OF NUMBER

AND ORIGINAL AMOUNT OF MEDIUM-TERM LOANS HELD BY

LENDING INSTITUTIONS AROUND 1940

COMMERCIAL

BANKS

60

40

20 0

LOAN SIZE CLASS

0

(in thousands)

Less than $10

10 — 50

50 — 100

100 — 250

250 — 500

500 — 1,000

1,000 — 5,000

5,000 — 10,000

10,000 and Over

LIFE INSURANCE

COMPANIES

20

40

60

Less than

10 —

50 —

too —

250 —

500,—

1,000 —

5,000 —

10,000

OF LOANS

____

AMOUNT OF LOANS

RECONSTRUCTION

FEDERAL

FINANCE CORPORATION

RESERVE

BANKS

60

40

20 0

0 20

40

60

$10

50

100

250

500

1,000

5,000

10,000

and Over

I__—

The largest number of loans made by public loan agencies

were in amounts less than $500,000; loans of life insurance

companies were primarily in excess of this amount. Commer-

cial bank loans were more diversified.

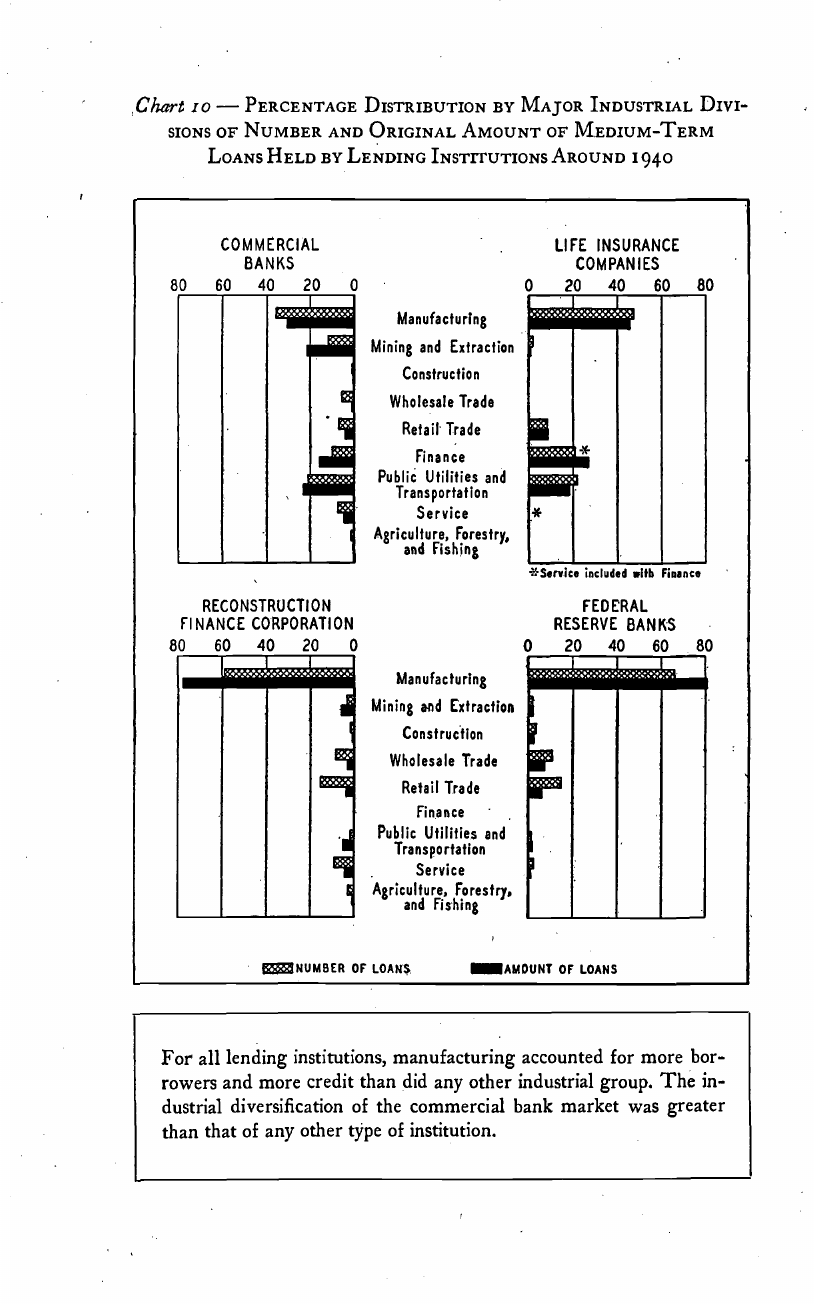

Chart io — PERCENTAGE

DIsnUBUTI0N BY MAJOR INDUSTRIAL Divi-

SIONS OF NUMBER AND ORIGINAL AMOUNT OF MEDIUM-TERM

LOANS HELD BY LENDING INSTiTUTIONS AROUND 1940

COMMERCIAL

LIFE INSURANCE

BANKS

COMPANIES

80 60

40

20 0

0 20

40

60

80

Manufacturing

I

Minng and Extraction

Construction

Wholesale Trade

Retail Trade

_____

Finance

Public Utilities and

•

Transportation

Service

I

Agriculture, Forestry.

and Fishing

RECONSTRUCTION

FINANCE CORPORATION

80 60

40

20 0

0

Manufacturing

Mining and Extraction

I

Construclion

•

Wholesale Trade

Retail Trade

Finance

Public Utilities and

Transportation

Service

Agriculture, Forestry.

—

_____ _____

and Fishing

•

OF LOANS

_I

*

included aith Finance

FEDERAL

RESERVE BANKS

20

40

60

80

I

AMOUNT OF LOANS

For

all lending institutions, manufacturing accounted for more bor-

rowers and more credit than did any other industrial group. The in-

dustrial diversification of the commercial bank market was greater

than that of any other type of institution.

BANKS AS SUPPLIERS OF CREDIT, 1940

57

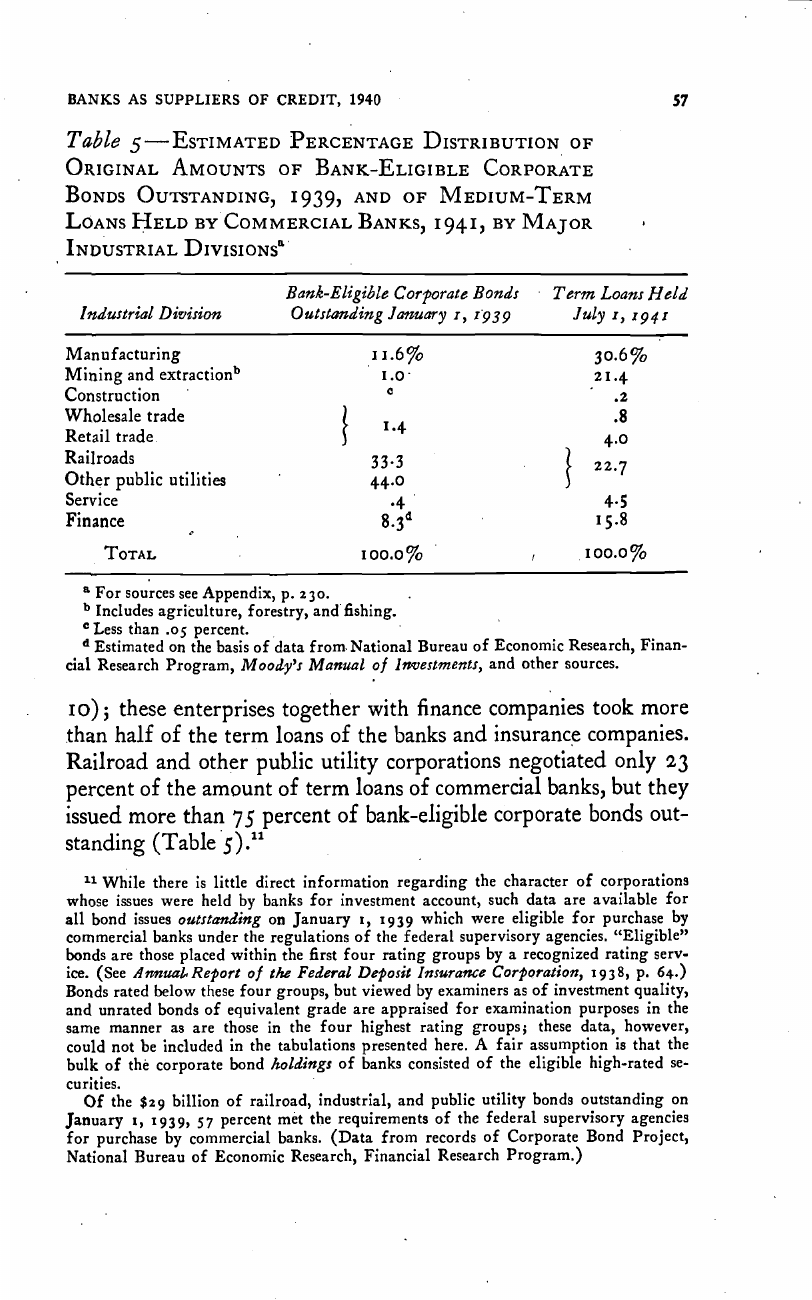

Table 5—ESTIMATED PERCENTAGE DISTRIBUTION OF

ORIGINAL AMOUNTS OF BANK-ELIGIBLE CORPORATE

BONDS

1939, AND OF MEDIUM-TERM

LOANS HELD BY COMMERCIAL BANKS, 1941, BY MAJOR

INDUSTRIAL DivIsIoNsa

Industrial Division

Bank-Eligible Corporate

Outstanding January r,

Bonds

1939

Te

rm Loans Held

July

Manufacturing

Mining and extractionb

ii.6%

1.0

30.6%

21.4

Construction

°

.2

Wholesale trade

Retail trade.

4

.

.8

4.0

Railroads

Other public utilities .

33.3 .

44.0

.

22.7

Service

.4

4.5

Finance

83d

. 15.8

TOTAL . ioo.o%

, .ioo.o%

a For

sources see Appendix, p. 230.

b Includes

agriculture, forestry, and fishing.

C

Less

than .05

percent.

d

Estimated on the basis of data from. National Bureau of Economic Research, Finan-

cial Research Program, Moody's Manual of investments, and other sources.

io); these enterprises together with finance companies took more

than half of the term loans of the banks and insurance companies.

Railroad and other public utility corporations negotiated only

percent of the amount of term loans of commercial banks, but they

issued more than 75 percent of bank-eligible corporate bonds out-

standing (Table

While

there is little direct information regarding the character of corporations

whose issues were held by banks for investment account, such data are available for

all bond issues outstanding on January i,

1939

which were eligible for purchase by

commercial banks under the regulations of the federal supervisory agencies. "Eligible"

bonds are those placed within the first four rating groups by a recognized rating serv-

ice. (See Annual.. Report of Me Federal Deposit Insurance Corporation, 1938, p. 64.)

Bonds rated below these four groups, but viewed by examiners as of investment quality,

and unrated bonds of equivalent grade are appraised for examination purposes in the

same manner as are those in the four highest rating groups; these data, however,

could not be included in the tabulations presented here. A fair assumption is that the

bulk of the corporate bond holdings of banks consisted of the eligible high-rated se-

curities.

Of the $29 billion of railroad, industrial, and public utility bonds outstanding on

January i,

1939,

57 percent met the requirements of the

federal supervisory agencies

for purchase by commercial banks. (Data from records of Corporate Bond Project,

National Bureau of Economic Research, Financial Research Program.)

58

BUSINESS FINANCE- AND BANKING

• CHARACTERISTICS OF MEDIUM-TERM AND

LONG-TERM LOANS TO BUSINESS

Significant differences existed before World War II between the

medium- and long-term loans of banks and of other credit institu-

tions. There were also differences between the direct and the open

market business loans of commercial banks with respect to the term

of the debt to its maturity, the type of security taken by the lender

to assure repayment, the use of the funds by the borrower, the pro-

visions for repayment, and the interest charged the borrower.

Maturity

The original term to maturity of corporate bonds eligible forpur-

chase by commercial banks around 1940 was considerably longer

than that of term loans made directly to business. Practically all the

amounts of corporate bonds were due after five years, whereas

approximately half of all term loan credit matured within five

years (Table 6). The majority of direct business loans of the RFC

also matured within five or ten years, while the maximum term of

Table 6—ESTIMATED PERCENTAGE DISTRIBUTION OF

ORIGINAL AMOUNTS OF BANK-ELIGIBLE CORPORATE

BONDS OUTSTANDING, 1939, AND OF MEDIUM-TERM

LOANS HELD BY COMMERCIAL BANKS, 1941, BY ORIGI-

NAL TERM TO MATURITYa

Original Term

to Maturityb

Bank-Eligible Corporate

Outstanding January i,

Bonds

1939

Term Lo€ms Held

July 1,194

I year

°

1.1%

1—3 .i% 13.0

3—5

.3 3.5.4

5—10

5.9

48.7

10—15 13.6

.6

15—20

6.z ..

2O—30 36.3 .

30—50 29.7 ...

Over 50

7.9 .•

No information

... 1.2

TOTAL

ioo.o%

a For

sources see Appendix, p. 230.

b

Each interval is exclusive of lower limit and inclusive of upper.

C

Less

than .05

percent. -

BANKS AS SUPPLIERS OF CREDIT, 1940

59

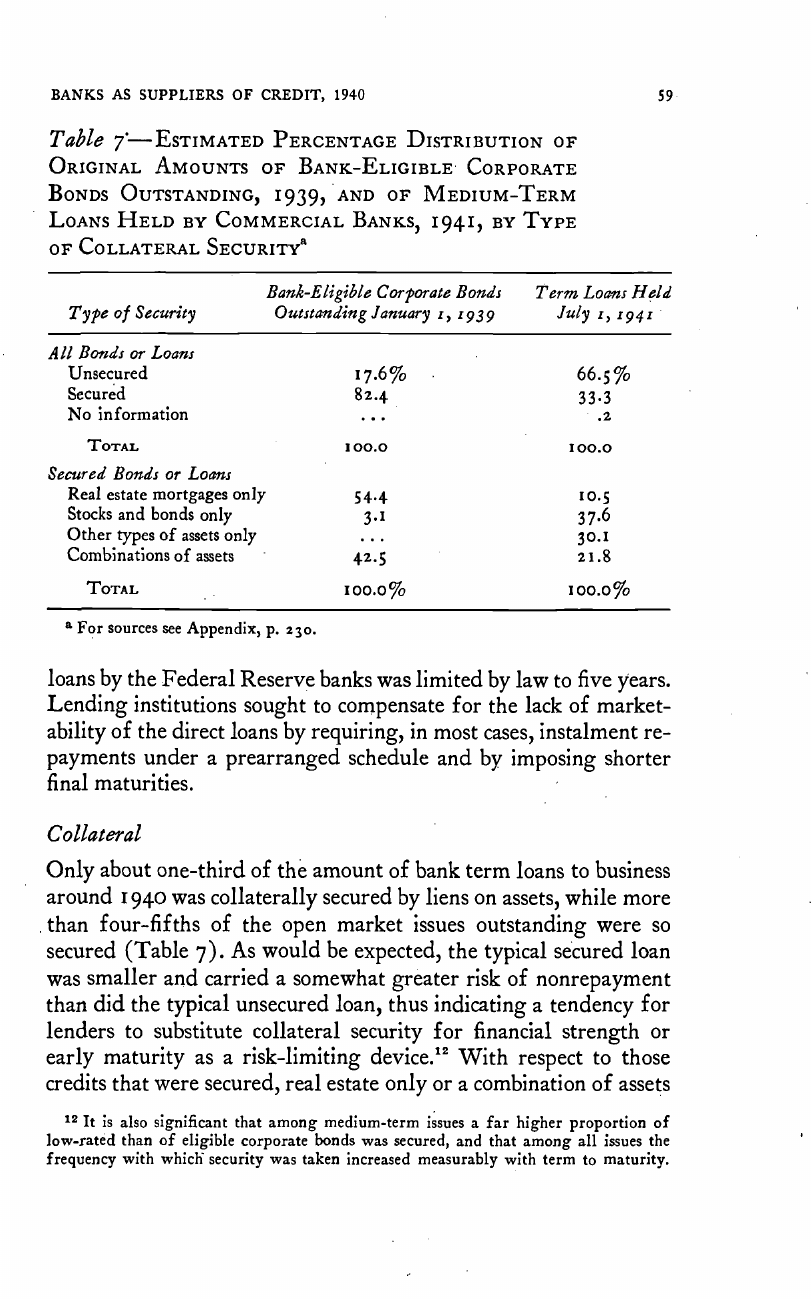

Table 7—ESTIMATED PERCENTAGE DISTRIBUTION OF

ORIGINAL AMOUNTS OF BANK-ELIGIBLE CORPORATE

BONDS OUTSTANDING, 1939, AND OF MEDIUM-TERM

LOANS HELD BY COMMERCIAL BANKS, 1941, BY TYPE

OF COLLATERAL

Type of Security

Bank-Eligible Corporate

Outstanding January i,

Bonds

1939

Term Loans Held

July 1,1941

All Bonds or Loans

Unsecured

Secured

No information

17.6%

82.4

..

.

.

:

33.3

.2

TOTAL

100.0

100.0

Secured Bonds or Loans

Real estate mortgages only

Stocks and bonds only

Other types of assets oniy

Combinations of assets

54.4

3'

. .

.

42.5

•

10.5

37.6

30.1

zi.8

TOTAL

ioo.o%

ioo.o%

a For

sources see Appendix, p. 230.

loans by the Federal Reserve banks was limited by law to five years.

Lending institutions sought to compensate for the lack of market-

ability of the direct loans by requiring, in most cases, instalment re-

payments under a prearranged schedule and by imposing shorter

final maturities.

Collateral

Only about one-third of the amount of bank term loans to business

around 1940 was collaterally secured by liens on assets, while more

than four-fifths of the open market issues outstanding were so

secured (Table 7). As would be expected, the typical secured loan

was smaller and carried a somewhat greater risk of nonrepayment

than did the typical unsecured loan, thus indicating a tendency for

lenders to substitute collateral security for financial strength or

early maturity as a risk-limiting device.12 With respect to those

credits that were secured, real estate only or a combination of assets

12 It is also significant that among medium-term issues a far higher proportion of

low-rated than of eligible corporate bonds was secured, and that among all issues the

frequency with which security was taken increased measurably with term to maturity.

60 BUSINESS FINANCE AND BANKING

was used more frequently as security under corporate bond inden-

tures, whereas single types of assets other than real estate were

more frequently pledged to secure term loans. Like bank term

loans, one-third of the amount of medium-term securities privately

purchased by life insurance companies was collaterally secured,

reflecting their prime quality as credit risks. In marked contrast, 83

percent of the business credit granted by the Federal Reserve

banks and virtually all that of the RFC was secured. The

agencies, dealing with borrowers unable to obtain accommodation

through private channels, were compelled to take every precaution

to assure repayment. A feature of the RFC loans was that com-

binations of assets were placed under lien in many instances.

Use of Fzinds

The majority of bank-eligible corporate issues around 1940 were

for both retirement and new money purposes, whereas bank term

loans were generally used exclusively for either one or the other

purpose (Table 8). Thus term loans served simplerfunctions in the

borrowing businesses, because they were of shorter term to maturity

and of smaller average amount. RFC loans were restricted by

statute to "maintaining or promoting the economic stability of the

country or encouraging the employment of labor," and the Cor-

poration announced that it would not lend money primarily to en-

able a borrower to repay existing debts. Federal Reserve bank loans

were limited by law to the provision of "working capital," which

precluded use of the proceeds for refunding, plant expansion, or

improvement.

Repayment Provisions

In regard to method of repayment, no less than 88 percent of the

amount of bank-eligible corporate bonds was repayable in one

lump sum at maturity, whereas about 85 percent of all term loan

debt was repayable in instalments, for the most part equal in amount

but in many instances with a final "balloon" note larger than its

predecessors. Serial bonds were relatively unimportant in open

market corporation financing, except in the financing of railroad

equipment. But approximately 17.5 percent of corporate bond issues

required annual purchases of outstanding debt through sinking

funds, thus reducing debt in the hands of the public periodically in

BANKS AS SUPPLIERS OF CREDIT, 1940

61

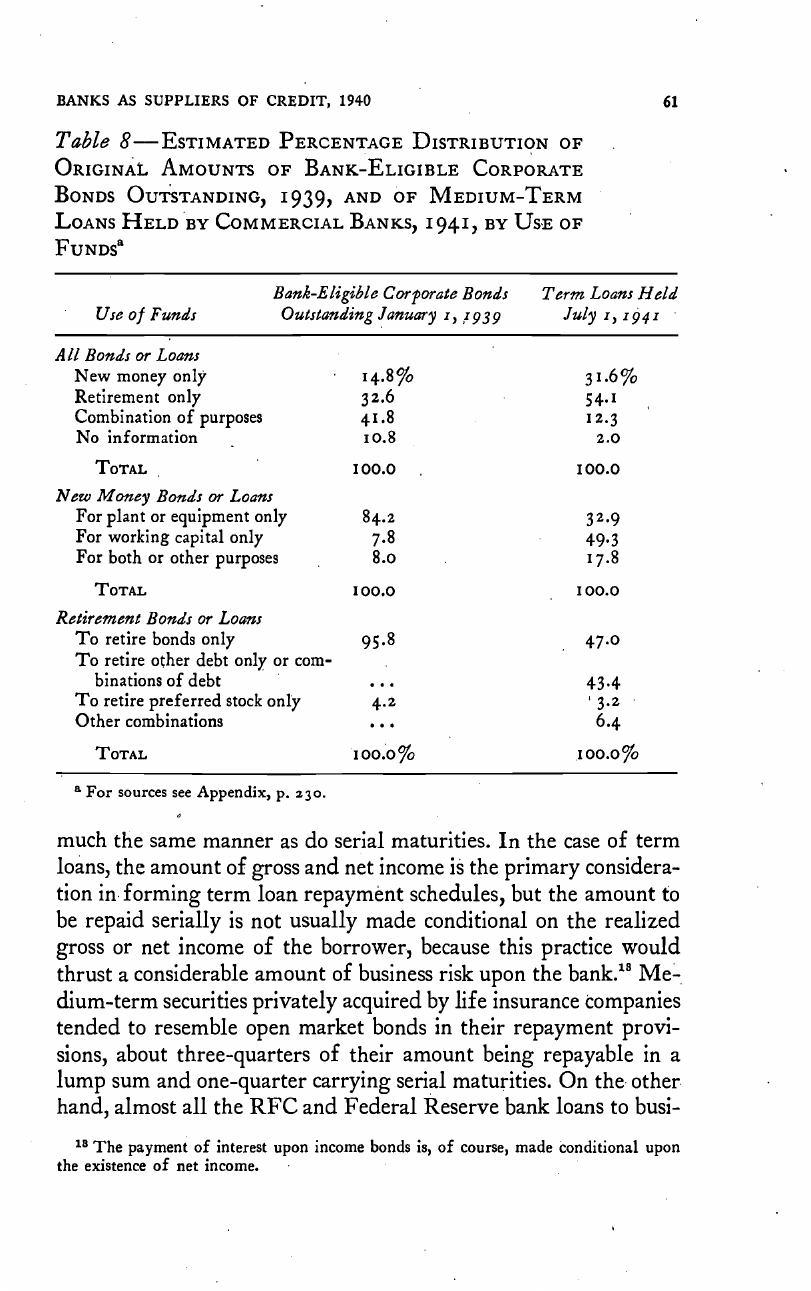

Table 8—ESTIMATED PERCENTAGE DISTRIBUTION OF

ORIGINAL AMOUNTS OF BANK-ELIGIBLE CORPORATE

BONDS OUTSTANDING, 1939, AND OF MEDIUM-TERM

LOANS HELD BY COMMERCIAL BANKS, 1941, BY OF

FUNDSa

Bank-Eligible Corpora

Use of Funds

Outstanding January

te Bonds

1939

T

erm Loans He

July z,

id

•

All Bonds orLoans

0

New money only 14.8% 31.6%

Retirement only 32.6

Combination of purposes 41.8 .

54.1

I 2.3

No information io.8 2.0-

TOTAL 100.0 100.0

New Money Bonds or Loans

For plant or equipment only 84.2

32.9

For working capital only

7.8

49.3

For both or other purposes

8.o

. 17.8

TOTAL

100.0

100.0

Retirement Bonds or Loans

To retire bonds oniy

95.8 47.0

To retire other debt only or corn-

binations of debt

... 43.4

To retire preferred stock only 4.2

3.2

Other combinations

... 6.4

TOTAL

ioo.o%

.ioo.o%

a For sources see Appendix,

230.

0

much

the same manner as do serial maturities. In the case of term

loans, the amount of gross and net income is the primary considera-.

tion in forming term loan repayment schedules, but the amount to

be repaid serially is not usually made conditional on the realized

gross or net income of the borrower, because this practice would

thrust a considerable amount of business risk upon the bank.13 Me-.

dium-term securities privately acquired by life insurance companies

tended to resemble open market bonds in their repayment provi-

sions, about three-quarters of their amount being repayable in a

lump sum and one-quarter carrying serial maturities. On the other

hand, almost all the RFC and Federal Reserve bank loans to busi-

The payment of interest upon income bonds is, of course, made conditional upon

the existence of net income.

62

BUSINESS FINANCE AND BANKING

ness were repayable in instalments, which were generally due

monthly or quarterly rather than annually. These requirements

undoubtedly reflected the close control that the lender to finan-

cially-straitened businesses finds it necessary to exercise in order to

protect his, position.

Interest Rates

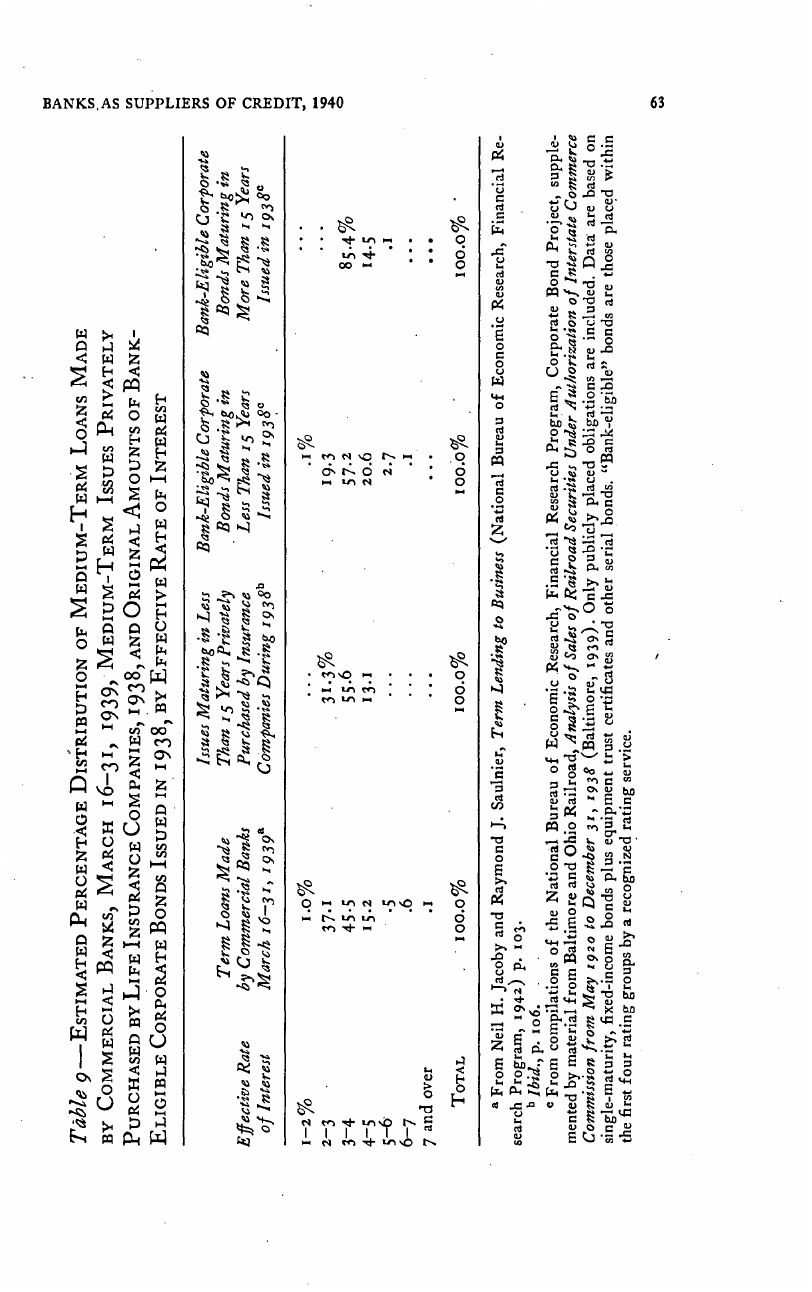

Nearly all term loan credit and long-term credit acquired under

bank-eligible corporate issues around 1940 cost the borrowers be-

tween 2 and c percent (Table 9). However, while 38 percent of

term loans were made at rates below 3 percent, all eligible corpo-

rate bonds maturing in more than ig years were issued at rates of 3

percent and over. Term loans, because of their smaller average size,

might be expected to carry a rate above that on corporate issues;

on the other hand, corporate issues, having an average term to ma-

turity longer than that for direct loans, might be expected to' carry

the higher rate. These two factors tended to, but did not completely,

offset one another, which accounts for the differential in average

interest rates.

The average charge by banks for medium-term and long-term

credit extended to business enterprises, it is significant to note, was

about equal to their average charge for short-term credit, the higher

quality and larger size of the long-term loans offsetting the shorter

life of the short-term loans. Likewise, among public lending

agencies rates tended to be about the same, regardless of final matu-

rity; for both RFC and Federal Reserve bank loans to business,

rates varied from

to

6 percent, depending mainly upon size,

industrial character, and credit standing of the borrower.

COMPETITIVE FORCES WITHIN THE MEDIUM-TERM

AND LONG-TERM BUSINESS CREDIT MARKET

In direct lending on medium and long.term during 'the years prior

to World War II, life insurance companies, commercial banks, and

government loan agencies —

the three principal types of institu-

tional suppliers of these types of credit to business —

served differ-

ent size groups of business. Life insurance companies provided both

medium-term and long-term loans primarily to large concerns;

banks provided credits of intermediate length to size groups of bor-

Issues Maturing in Less

Bank-Eligible Corporate

Bank-Eligible Corporate

Term Loans Made

Than 15

Years Privately

Bonds Maturing in

Bonds Maturing in

Effective Rate by Commercial Banks

Purchased by Insurance

Less Than Years

More Than 15

Years

of Interest March 16—31, 59395

Companies During

Issued in

Issued

1938C

5—2% i.o% ...

.i% ...

2—3 37.1

31.3% 19.3 .

3—4 45.5

55.6

57.2

85.4%

4—5

55.2 13.1 20.6

'4.5

5—6

.5 . .

.

2.7 .1

6—7

.6 ...

.1 ...

7andover

.1 ...

... ...

TOTAL ioo.o% ioo.o% ioo.o% - ioo.o%

a From

Neil H. Jacoby and Raymond J. Saulnier, Term Lending to Business (National Bureau of Economic Research, Financial Re-

search Program, 5942)

p.

103.

blbjd.,p.

io6.

From compilations of the National Bureau of Economic Research, Financial Research Program, Corporate Bond Project, supple-

mented by material from Baltimore and Ohio Railroad, Analysis of Sales of Railroad Securities Under Authorization of Interstate Commerce

Commission from May 1920 to December 31,

5938

(Baltimore, 1939). Only publicly placed obligations are included. Data are based on

single-maturity, fixed-income bonds plus equipment trust certificates and other serial bonds. "Bank-eligible" bonds are those placed within

the first four rating groups by a recognized rating service.

Table 9—ESTIMATED PERCENTAGE OF MEDIUM-TERM LOANS MADE

BY COMMERCIAL BANKS, MARCH 16—31, 1939, MEDIUM-TERM ISSUES PRIVATELY

PURCHASED BY LIFE INSURANCE COMPANIES, 1938, AND ORIGINAL AMOUNTS OF BANK-

ELIGIBLE CORPORATE BONDS ISSUED IN 1938, BY EFFECTIVE RATE OF INTEREST

z

In

In

'0.

'0

In

0

'TJ

'C

64

BUSINESS FINANCE AND BANKING

rowers ranging from very small to very large, but the bulk of this

credit went to concerns of medium size; the government loan

agencies served medium-sized and small businesses.

In medium- and long-term lending, the intensity of inter-agency

competition was great in the making of large loans to the larger

businesses possessing impeccable credit ratings. Banks and insurance

companies competed actively for such business, which drove down

the loan rate. In the making of medium-term loans to small busi-

nesses, inter-agency competition was less intensive, because the pri-

vate lending institutions often considered the risks and costs of

lending to this clientele too high relative to the rates which they

could (or would) charge. Medium-term credit, in practice, was

available to many small businesses only at, or with the participation

of, the Reconstruction Finance Corporation or the Federal Reserve

banks. To the extent that public regulation of banks and life insur-

ance companies discouraged the assumption of credit risks, such

regulation served, of course, to intensify competition for the large,

prime loans and to reduce it for small loans.

A number of factors account for the substantial fraction of long-

term credit to business procured directly from a lending institution

in 1940 rather than indirectly through a public offering of bonds

or notes —

even by large concerns able to use either method. In the

first place the costs of making a public offering were numerous and

onerous. They included expenses imposed upon issuers by the Secu-

rities Act of 1933, underwriters' commissions, costs of advertising,

the printing of registration statements and prospectuses, the en-

graving of certificates or bonds, transfer taxes, and costs of listing

the new securities on exchanges and of maintaining transfer facili-

ties. But the greater speed and flexibility of direct financing versus

open market financing may have weighed as heavily as cost con-

siderations. Compared with public issues, direct loans had the advan-

tage of rapid negotiation and expeditious modification to meet

changed circumstances. Direct loans also offered the advantages of

requiring no special public disclosures of corporate affairs, and of

freeing directors of the borrowing corporation from the civil

liabilities they would carry if

public offering were made.

But the public offerings possessed special advantages of other

kinds. They could broadly establish the credit of the borrowing con-

cern, enabling it to obtain lower interest rates in future financing.

Wide distribution of the debt of the borrowing business could

BANKS AS SUPPLIERS OF CREDIT, 1940

65

enable the concern occasionally to repurchase and retire debt on

advantageous terms. The choice between open market and direct

borrowing appeared to be based upon a weighing of alternative

costs and advantages in the light of the borrowing business' circum-

stances.

STAKE OF COMMERCIAL BANKS IN FINANCING

OPERATIONS OF NONFINANCIAL BUSINESS

A surprisingly small percentage of the total. earning assets of the

commercial banking system at the end of 1940 represented out-

standing credit to nonfinancial business enterprises. The amount of

such credit is estimated at about $10.3 billion, or less than 25percent

of the total earning assets of

billion held at that time by all

operating insured banks. Loans to nonfinancial business were only

half as important as federal, state, and local government securities,

and about equal in importance to the aggregate amount of credits

extendel to security dealers, agriculture, consumers, and nonprofit

institutions. Thus, well before the necessities of war had inflated

federal borrowings from, the banks, government as a banking cus-

tomer was twice as important as business,

agriculture and

security dealers. Wartime federal financing only accentuated this

condition.14

About $7.7 billion or three-fourths of all bank credit to non-

financial business took the technical form of "loans and discounts,"

and the balance of $2.6 billion was investment in C(securities " This

distinction does not break down nonfinancial business credit into

short-term and long-term advances, nor into credit extended

through the open market and that granted directly. The data in

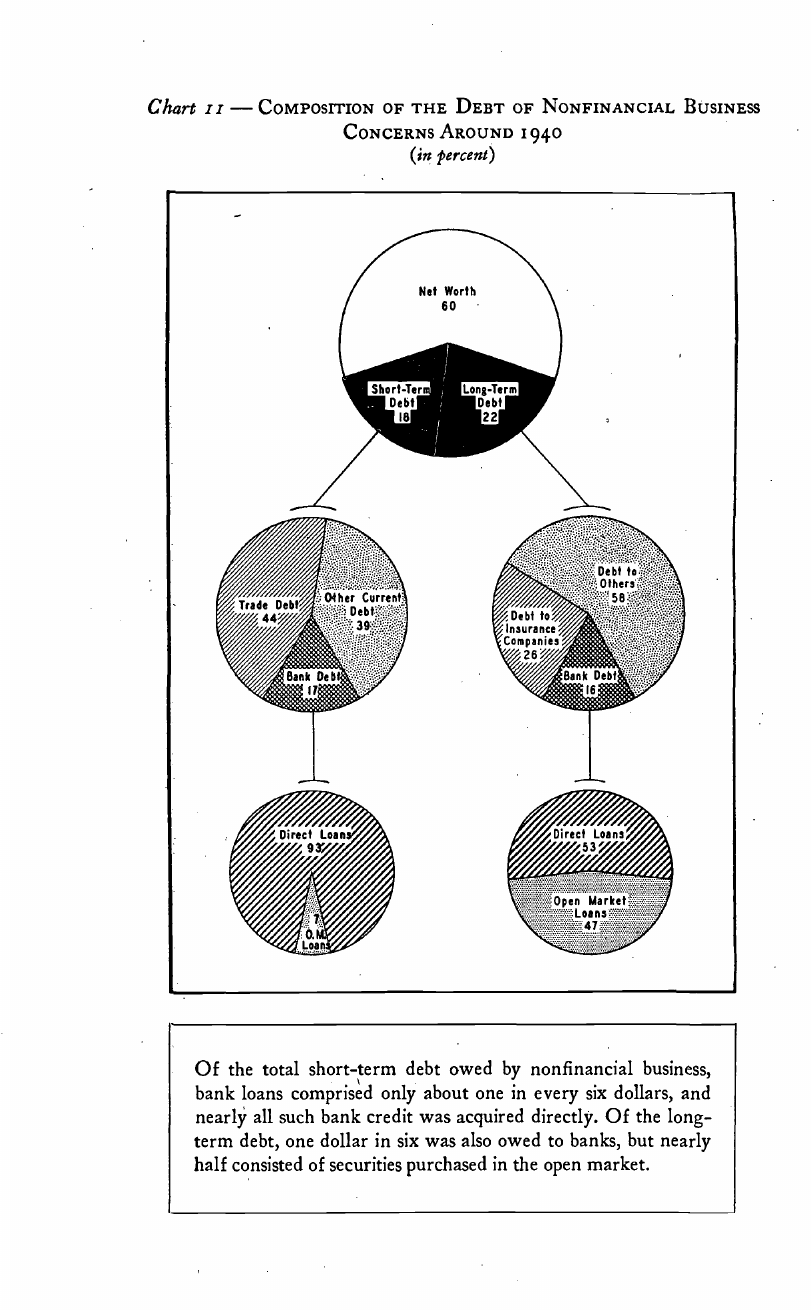

Chart I I are classified along these lines and reveal the astonishing

fact that nearly half of all bank credit to nonfinancial business was

long-term in character, maturing more than a year after being con-

tracted. This measures the extent to which banks had departed by

1940 from the short-term self-liquIdating business advance sanc-

14 The large role which direct consumer financing had come to play in banking

operations by the end of 1940 was also of great significance. Consumer credit, com-

prising instalment loans arid home mortgage loans, amounted to about

billion,

or nearly one-half of outstanding business credit. Consumer instalment loans as of the

end of 1940 are estimated by the ,National Bureau of Economic Research, Financial

Research Program, as approximately

billion. The Annual Report of the Federal

Deposit Insurance Corporation, 1940, p.

145, records loans secured' by residential

property amounting to $2.9 billion.

Chart ii — CoMPosrrloN

OF THE DEBT OF NONFINANCIAL BUSINESS

CONCERNS AROUND 1940

percent)

Of the total short-term debt owed by nonfinancial business,

bank loans comprised only about one in every six dollars, and

nearly all such bank credit was acquired directly. Of the long-

term debt, one dollar in six was also owed to banks, but nearly

half consisted of securities purchased in the open market.

BANKS AS SUPPLIERS OF CREDIT, 1940

67

tioned by the classical theory of banking. Of equal interest was the

great difference between the relative importance of open market and

direct loans. Nearly

93 percent of short-term bank credit to non-

financial business was extended directly to the borrower, while only

53

percent

of long-term credit was so transmitted.15 The minor

importance in the United States of open market dealings in the

short-term debts of nonfinancial business concerns contrasts strongly

with market conditions for trade bills and acceptances in British

finance. Likewise, the extent to which American banks purchased

directly the long-term obligations of business enterprises is notable

in comparison with British practices.

From the point of view of the gross revenue it produced, credit

extended to nonfinancial business was a more important aspect of

commercial banking than the relation of such loans to total Ccearning

assets" suggests. Available data do not reveal the amount of banks'

gross earnings from loans to nonfinancial business. They show only

gross earnings from loans of all kinds and from investments in

securities of all kinds, thus mingling business concerns with other

borrowers. From these data it is known that for banks, on the

average, the gross revenue collected from each dollar of loans in

1940 was about twice that collected from each dollar of invest-

ments, the figures being respectively 4.18

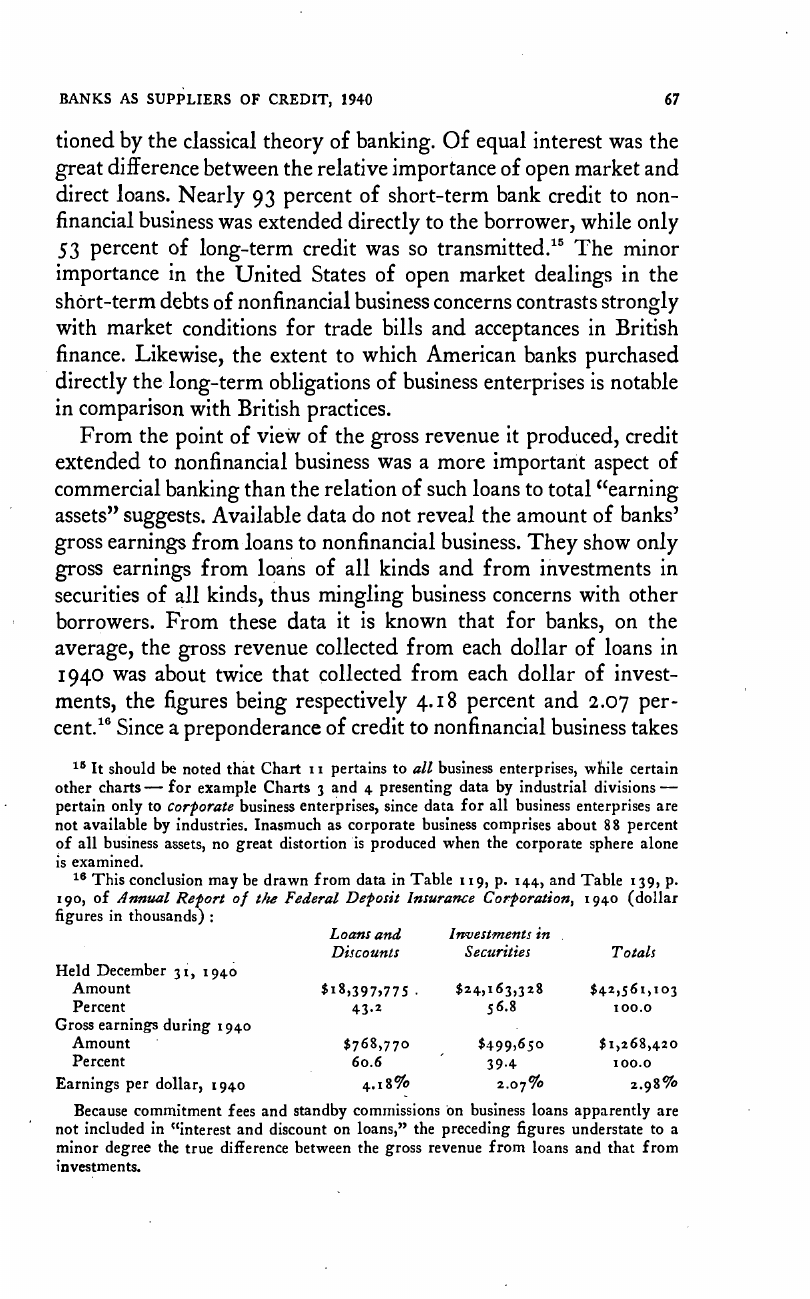

percent

and 2.07 per-

cent.'6 Since a preponderance of credit to nonfinancial business takes

It should be noted that Chart i i pertains to all business enterprises, while certain

other charts — for

example Charts 3 and 4 presenting data by industrial divisions —

pertain

only to cor/'orate business enterprises, since data for all business enterprises are

not available by industries. Inasmuch as corporate business comprises about 88 percent

of all business assets, no great distortion is produced when the corporate sphere alone

is examined.

16

This conclusion may be drawn from data in Table 119,

p.

144, and Table i

39,

p.

I 90, of Annual Report of the Federal Deposit Insurarwe Corporation, 1940 (dollar

figures in thousands):

Loans and

Investments in

Disco unis

Securities Totals

Held December 31,

1940

Amount

$18,397,775 .

$24,163,328

$42,561,103

Percent

43.2

too.o

Gross earnings during 1940

Amount

$768,770 $499,650 $1,268,420

Percent 6o.6

39.4

100.0

Earnings per dollar, 194o 4.18%

2.07%

2.98%

Because commitment fees and standby commissions on business loans apparently are

not included in "interest and discount on loans," the preceding figures understate to a

minor degree the true difference between the gross revenue from loans and that from

investments.

68

BUSINESS FINANCE AND BANKING

the form of loans and a preponderance of other credit takes the

form of securities, the former as a whole produced a higher rate of

gross income per dollar than did the latter as a whole. When allow-

ance is made for the somewhat higher effective yield of corporate

bonds than of government security holdings, it may be concluded

that roughly one-third of the gross earnings of banks from all

credit operations accrued from business credit.17 Nothing can be

said with certainty concerning the net profitability to banks of any

type of lending operation in 1940, because banking costs are not

commonly broken down between loans and investments of different

kinds.

The extent of the financing of nonfinancial business enterprises

in 1940 was not, of course, the same for all commercial banks. The

stakes of individual banks differed according to: the size of the

banks, the size of the centers in which they were located, the eco-

nomic character of the territories, and banks' operating policies.

Broadly speaking, business loans formed relatively high percent-

ages of the total assets of medium-sized banks with total deposits

between $500 thousand and $io million. In many instances these

banks were located in cities where diversified industrial activity

made the demand for business credit most active. Agricultural

credits comprised a large percentage of the total loan portfolios of

small banks, since these banks usually served agricultural areas or

were located in small population centers where local demands for

business credit were not extensive. Mortgage loans secured by resi-

dential and other property formed a substantial proportion of the

loan portfolios of banks with assets of over $10 million, except those

in central money markets. Nevertheless, divergencies among banks

in the importance of business financing activities were not strikingly

large prior to World War II.

1? In making this estimate, gross earnings from commissions, fees, collection, ex-

change, and service charges, and other current operating earnings have been excluded,

although some part of these earnings of banks is certainly attributable to their loan

and investment activities. If income trust, collection, exchange, and other serv-

ices

is

included, total gross current operating earnings of all insured operating

commercial banks during 1940 amounted to $1,631,074,000. (See Annual Report of

the Federal Deposit Insurance Corporation, i94o, Table 139, p. '9°.) Of this total,

business credit may be roughly estimated to have produced $374,809,000, or 23 per-

cent.